The year 2023 has proven quite inflationary, as a confluence of factors has driven up the prices of goods and services globally. Supply chain disruptions lingering from the pandemic, tight labor markets, pent-up consumer demand, and expansive fiscal policies have all contributed to inflation, reaching 6.9% in September.[1]

Economists remain divided on whether this inflation will be transitory or persistent. Optimists argue that as economies continue recovering ground lost to COVID-19, prices will stabilize. Pessimists counter that inflation may take on a rife of its own if wages cannot keep pace and erode consumer purchasing power.

A pressing question is how employee compensation is adapting to this high-price environment. Can workers’ paychecks purchase the same volume of necessities as before? Or will stagnant incomes relative to inflation shrink real wages and living standards? The answers have implications for the growth trajectories of nations and present challenges for governments and central banks aiming to tame inflation without stalling economic activity.

Wages Vs. Inflation: A Mixed Picture?

The link between what people earn and price rises is complex. Wages should normally go up with inflation so paychecks buy the same stuff. But sometimes wages don’t keep up with prices for different reasons.

Like how busy companies are, how fast new things get made, how hard it is to ask for more pay, and rules in place.

The UN recently found that in 2022, wages went up 7.8% worldwide but prices went up more at 8.2%. So paychecks could buy less stuff. In theory, at least. This hasn’t happened for a long time.

It was different in richer countries though. Wages rose 8.1% and prices 7.4% so paychecks kept their value. This shows their economies are getting better after COVID. Places like the US and UK also had a hard time filling jobs, so companies had to pay more.

Poorer countries saw wages rise 7.6% but prices 9.1%. So paychecks lost value there. Their economies are recovering slower from COVID and have less help from governments. Countries like Argentina, Türkiye, and Nigeria also saw money problems, making imports cost more.

Also Read: How Big of a Failure Is “Make in India”?

Income Inequality Presents A Widening Gap

According to the research I found online, high inflation tends to impact lower-income individuals and families the hardest. That’s because those with fewer financial resources typically spend a greater portion of their earnings on essentials like food, utilities, rent, and transportation – all of which have experienced above-average price hikes in recent months.

Those with higher incomes have more flexibility in their budgets and are better able to absorb increasing costs. They also are more likely to have savings, investments, or other assets that can help offset inflation. In contrast, many low-income households live paycheck to paycheck without substantial cushions or ways to grow their money.

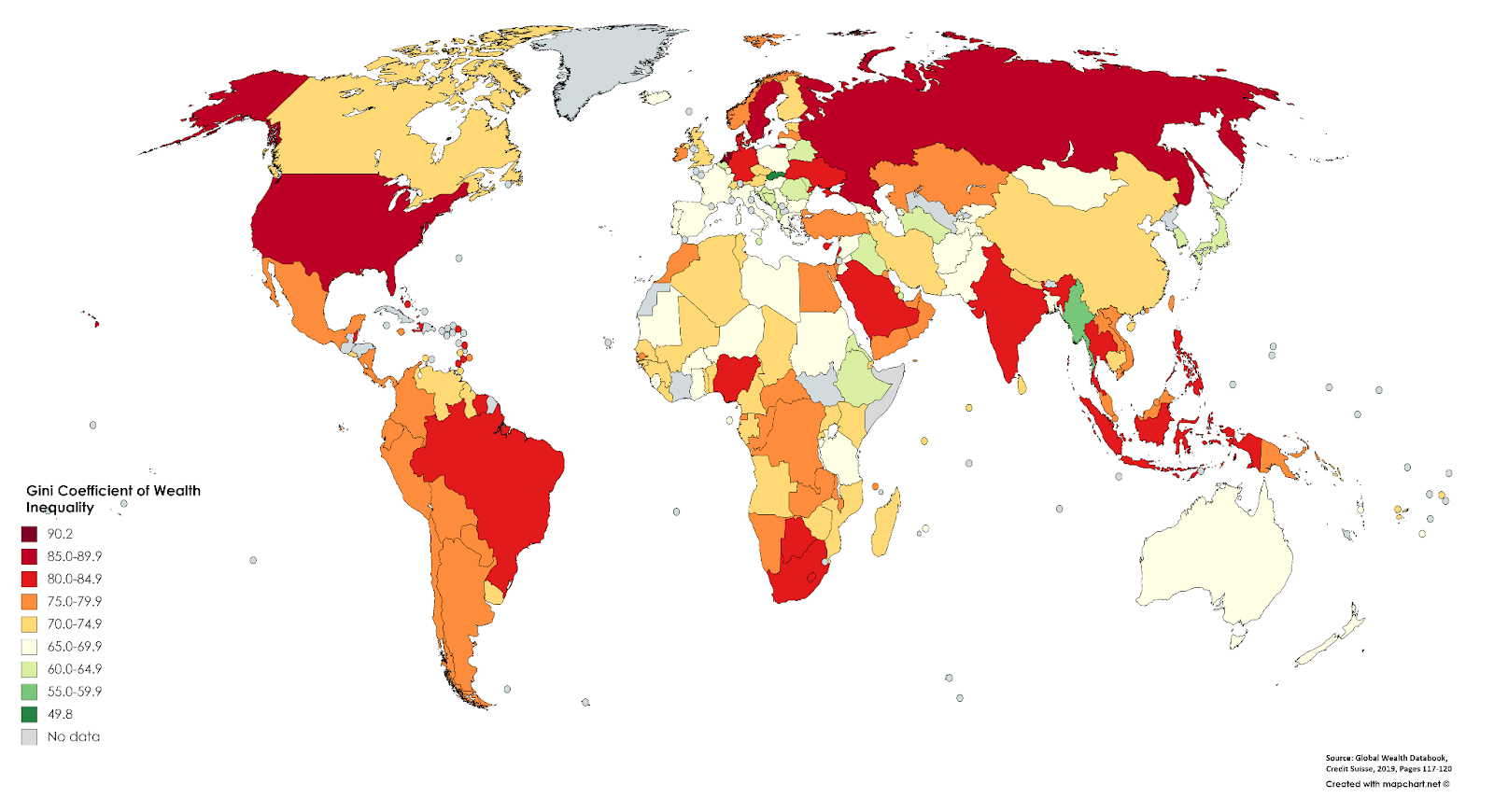

The World Bank predicts global poverty will rise in the aftermath of the pandemic as well. They estimate about 40 million more individuals worldwide could fall below the extreme poverty line of $1.90 per day due to economic difficulties raising the cost of basic needs. Income inequality is also expected to worsen according to the Gini coefficient measure.

Developed and developing countries have felt the impacts unevenly too (except for maybe India). Advanced nations saw quicker economic and employment recoveries thanks to larger vaccination campaigns and fiscal stimulus. Emerging markets faced bigger setbacks managing public health crises and the resulting financial strain. This has caused the gap in average incomes between the two country groups to expand after years of slow convergence.

Economic Growth

The high-price era can also impact economies in several ways. Higher wages may boost consumer spending and drive more business activity. But rising costs can reduce purchasing power and real incomes for both households and companies, slowing things down.

The IMF says global growth rebounded strongly in 2021 to its fastest pace since the 1970s after the pandemic hit in 2020. However, they note uncertainty remains high. Inflation poses challenges for monetary and fiscal policymakers.

Central banks face a dilemma. Raising interest rates curbs inflation but may slow recovery by making loans pricier. Keeping rates low supports growth but risks fueling inflation expectations. The right move depends on why and how long prices are increasing. It also varies by each bank’s flexibility and independence.

Governments must weigh stimulus versus stability. Spending more boosts growth but risks bigger deficits and debt loads, which could increase borrowing costs during crises. Cutting spending consolidates finances but weakens recovery and hurts low-income groups. The optimal response relies on a nation’s fiscal strength and priorities, plus coordination globally.

Outlook: Growth To Slow Further, Inflation Pressures To Ease

Most experts predict the global economy will slow further in 2024. The IMF expects world GDP growth to ease to 2.7% next year.

However, inflation may finally start to moderate from very high rates later in 2024. Supply chain issues are gradually improving and energy prices have fallen from peaks as oil production increases. The effect of higher interest rates should also help cool demand and bring consumer prices closer to central bank targets of around 2%.

Everything depends on whether inflation proves more persistent or if recession risks rise significantly. Geopolitics like the war in Ukraine and China’s COVID policies continue affecting global trade too. Overall wage growth exceeding inflation should support household incomes, but inequality issues persist without solutions.

For now, the high-price era will keep testing economies and social cohesion worldwide.